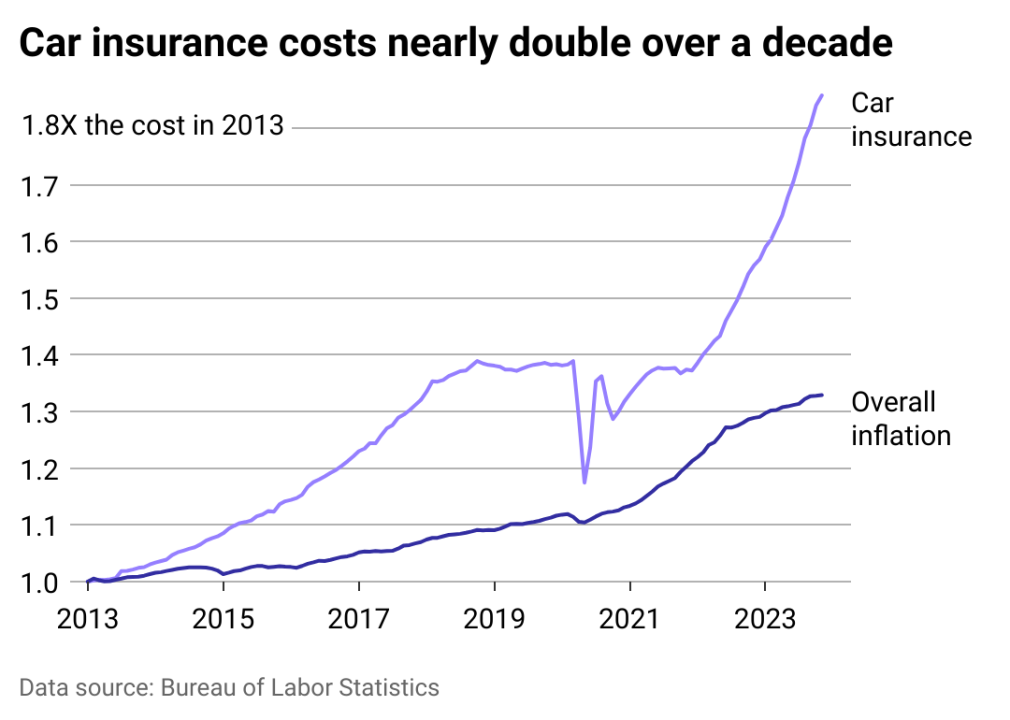

Car insurance costs are finally finding their footing in 2026, following a three-year stretch where premiums surged at nearly six times the rate of overall inflation. While the era of 17% annual hikes is behind us, the market remains at a historic high. Data from early 2026 shows a shift from a “catch-up” phase to a period of “structural complexity.”

While many major insurers have returned to profitability and are now competing for customers with modest rate cuts, the underlying cost of a single claim remains at a record high. CheapInsurance.com has identified the five evolving factors that are keeping premiums “sticky,” even as general inflation cools to 2.4%.

As Featured in

1. The Paradox of Safer Roads and Costlier Crashes

We are seeing a historic shift in 2026: traffic fatalities have dropped significantly, reaching their lowest levels since 2014. However, for insurance companies, “safer” hasn’t meant “cheaper.” While we are getting better at surviving crashes, our cars are not.

Dangerous behaviors like major speeding (up 16% since 2019) and distracted driving persist, and when these high-speed errors occur, they are devastating to modern vehicle frames. In 2026, nearly 29% of all collision claims result in the car being declared a “total loss”—a record high. Insurers are essentially paying out the full value of a vehicle more often than ever before, which keeps everyone’s premiums elevated despite the overall drop in roadway deaths.

2. High Repair and Replacement Costs

One of the biggest reasons insurance costs are rising is that cars have become much more expensive to fix. Several trends are driving this:

Complex vehicle technology

Today’s vehicles are packed with cameras, sensors, and driver-assistance features. These tools improve safety, but they also make repairs more complicated. Even a small accident can require recalibrating multiple systems, which quickly increases the repair bill.

Labor and parts shortages

Supply chain challenges and ongoing parts shortages—especially for microchips—have made repairs more expensive and slower. At the same time, there’s a shortage of skilled technicians, which pushes labor costs higher.

Inflation

Like everything else, the cost of materials, parts, and labor has increased in recent years, and those higher repair costs eventually affect insurance premiums.

3. More Severe Weather Events

Severe weather is another major factor. Storms, floods, hurricanes, and hail events are happening more often and causing more damage to vehicles. A single large storm can generate thousands of claims at once. In areas that face frequent disasters, insurers may raise rates significantly—or reduce the coverage they offer—to manage their risk.

Do You Need Collison and Comprehensive Coverage?

Fausto Bucheli Jr, licensed insurance broker and owner of CheapInsurance.com recommends: “Collision and comprehensive coverage should protect your financial stability. If your car is older and paid off, adjusting or removing these coverages can reduce your car insurance costs by hundreds of dollars per year without increasing financial risk.”

4. Rising Medical and Legal Costs

Vehicle theft has also become more costly, especially with the surge in catalytic converter theft across the country. Replacing one can cost thousands of dollars, and insurers typically cover the loss under comprehensive coverage. As these claims increase, they add another layer of pressure on insurance rates.

CheapInsurance.com by the Numbers

Data Analysis: Annual Savings from Car Insurance Comparison Sites

Founded in California in 1974 as an insurance agency, CheapInsurance.com has spent decades helping people find affordable coverage. Over time, we became one of the first brokerages to go online in 1998, making insurance shopping faster and easier.

Our mission has always been simple: insurance is a basic necessity, not a luxury. That’s why our technology quickly scans the marketplace in seconds, compares rates, and uncovers discounts that might otherwise be missed. In addition, we explain coverage in clear, simple terms.

As a result, people get real options and can avoid overpaying for features they do not need, while still maintaining strong, reliable protection.

Frequently Asked Questions About Rising Car Insurance Costs

Why are car insurance rates increasing faster than inflation?

Car insurance rates are rising faster than overall inflation due to higher vehicle repair costs, expensive medical claims, and more severe accidents. Advanced technology in vehicles also increases the cost to repair and replace damaged parts.

Which factors are driving these cost increases?

Key factors include more frequent and severe accidents, higher medical and repair costs, increased vehicle values, and inflation affecting auto parts and labor. These elements all contribute to higher insurance claims and rates.

How can I manage or reduce my car insurance costs?

You can reduce car insurance costs by comparing multiple quotes, maintaining a clean driving record, raising your deductible, bundling policies, and qualifying for discounts for safe driving, vehicle safety features, or low annual mileage.

Story editing by Ashleigh Graf. Copy editing by Kristen Wegrzyn.

By

Published

Reviewed By