Georgia drivers know the frustration of rising car insurance costs. But just how much have rates climbed since the 1980s, and what’s driving this seemingly relentless trend? In this article Cheapinsurance.com dives into the reasons behind the history of Georgia car insurance price increases and explores ways to navigate the current landscape.

Key Takeaways:

- Georgia car insurance rates have likely increased significantly since the 1980s, mirroring a national trend.

- Factors like rising accident rates, medical costs, and car repair expenses contribute to higher premiums in Georgia.

- Compared to some states, Georgia’s “fault” system and specific risk factors like weather events can impact insurance costs.

- Georgia drivers can manage costs by comparing rates, maintaining a clean record, and adjusting coverage levels.

- Future trends like autonomous vehicles and safety technology may influence car insurance prices in Georgia. Staying informed can empower you to make informed decisions.

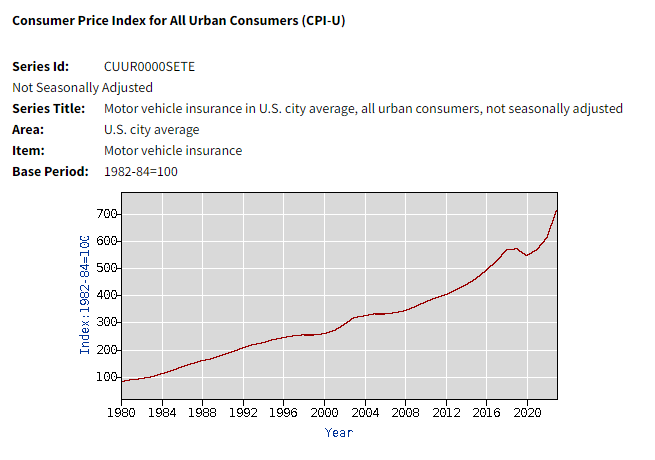

National Insurance Costs Since 1980

In our May 2020 reporting on How auto insurance rates have changed over the past decades we observed the following national car insurance premium trends based on U.S. Bureau of Labor Statistics data:

1980s

– Average monthly insurance premium: $119

– Premium increase from start of decade: $85 (103%)

1990s

– Average monthly insurance premium: $225

– Premium increase from start of decade: $76 (43%)

2000s

– Average monthly insurance premium: $315

– Premium increase from start of decade: $100 (39%)

2010s

– Average monthly insurance premium: $464

– Premium increase from start of decade: $196 (52%)

2020s

– Average monthly insurance premium: $564

– Premium increase from start of decade: $38 (7%)

How Affordable Was Car Insurance in Georgia During the 1980s?

Compared to today’s costs, car insurance in Georgia during the 1980s was significantly more affordable. Anecdotal evidence and historical data suggest drivers could paid several hundred dollars less annually for minimum liability coverage than they do today.

Here’s some perspective: According to U.S. Bureau of Labor Statistics data, the monthly national average cost of auto insurance at the end of 1989 was $119, which was a remarkable 103% increase over the $85 per month cost for car insurance at the start of the decade in 1980.

What Factors Have Driven Up Car Insurance Costs in Georgia?

Several key factors contribute to the rising cost of car insurance in Georgia:

- Increased Accident Rates: Data from the Georgia Department of Transportation (Georgia DOT) reveals a rise in traffic accidents over the past few decades. This translates to more insurance claims, putting pressure on insurers to raise premiums.

- Rising Medical Costs: Medical expenses associated with car accidents have skyrocketed. The cost of treatments, hospital stays, and rehabilitation are factored into insurance payouts, leading to higher rates in Georgia.

- More Expensive Cars & Repair Costs: Modern vehicles are packed with advanced safety features and complex technology. While this improves safety, it also drives up repair costs after an accident. Replacing these components can be expensive, leading insurers to adjust premiums accordingly.

- Distracted Driving: The rise of smartphones and in-car technology has contributed to a surge in distracted driving in Georgia. This reckless behavior increases the likelihood of accidents, prompting insurers to raise rates to offset the risk.

- State-Specific Regulations: Georgia operates under a “fault” insurance system. This means the at fault driver’s insurance company typically covers damages. While this aims to streamline claim processing, it can also lead to more lawsuits as drivers and their insurers fight over who is responsible, impacting insurance costs.

How Do Today’s Georgia Car Insurance Rates Compare to the National Average?

According to Bankrate, the average annual auto insurance premium in Georgia is $2,610. This is $67 more than the national average, placing Georgia at the number 35 spot on the list of states with the highest auto insurance costs. Georgia residents can expect to spend about 3.58% of their income on car insurance annually.

How Does Georgia’s Car Insurance System Compare to Other States?

While Georgia drivers face rising costs, it’s important to understand the national context. Here’s how Georgia’s car insurance system stacks up against other states:

- Fault vs. No-Fault: Unlike some states with “no-fault” systems, Georgia has a “fault” system. This can lead to more lawsuits and potentially higher premiums compared to no-fault states.

- National Trends: The national trend of rising car insurance costs also applies to Georgia. However, the exact increase might vary depending on factors like a state’s specific regulations, accident rates, and medical costs. Resources from the NAIC can provide a broader perspective on national car insurance trends.

- State-Specific Factors: While national trends influence Georgia, factors specific to the state also play a role. Georgia’s growing population, traffic congestion, and weather events (like hailstorms that can damage vehicles) contribute to higher premiums compared to states with different demographics or risk profiles.

While Georgia might not be an outlier in terms of rising car insurance costs, the state’s specific factors and fault-based system contribute to its current landscape.

Are There Ways to Reduce Car Insurance Costs in Georgia Today?

Even with rising costs, there are ways for Georgia drivers to manage their car insurance expenses:

Maintain a Clean Driving Record: Traffic violations including speeding tickets, and accidents significantly increase premiums. Too many infractions and accidents could result in the need for an SR-22 requirement. Practice safe driving habits and avoid distractions.

Increase Your Deductible: A higher deductible lowers your car insurance premium. However, choose a deductible you can comfortably afford in case of an accident.

Consider Usage-Based Insurance: Telematics programs offered by some car insurance companies track driving behavior and reward safe drivers with discounts.

Bundle Your Insurance: Bundling your auto insurance with your homeowners insurance or renters insurance can often lead to a discount.

Review Your Coverage: Regularly assess your coverage needs. If your car is older or has low value, consider dropping comprehensive coverage.

Take Advantage of Low Mileage Discounts: Some auto insurance companies offer discounts for drivers who drive fewer miles annually.

Ask About Available Discounts: Many insurance companies offer car insurance discounts for things like good student discounts, senior citizen discounts, military discounts, and defensive driving courses.

Maintain Your Car: Regularly maintaining your car can help prevent accidents and breakdowns, potentially leading to discounts from some insurers.

Consider Usage-Based Insurance: If you’re a safe driver, usage-based insurance can be a great way to save money. These programs track your driving habits (such as mileage, braking, and acceleration) and offer discounts to safe drivers.

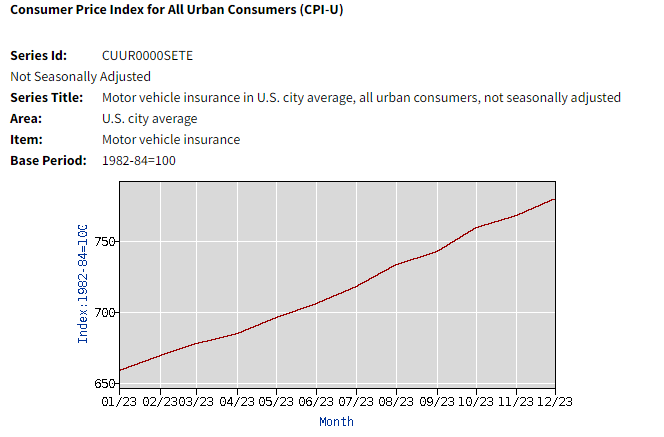

The Recent National Trend

In 2023 the U.S. Bureau of Labor Statistics reports that the national average annual auto premium increased from $658.51 in January 2023 to $780.28 in December 2023. The average annual auto insurance premium for all of 2023 was $716.00, with the first half of 2023 coming in at $681.76, and the second half at $750.24.

What Does the Future Hold for Car Insurance Costs in Georgia?

Predicting the future of car insurance costs is challenging, but several trends could impact Georgia drivers:

- Autonomous Vehicles: The widespread adoption of self-driving cars has the potential to significantly reduce accidents, potentially leading to lower car insurance rates in the long run. However, the timeline for widespread adoption remains uncertain.

- Technology and Accident Prevention: Advancements in safety features like automatic emergency braking and lane departure warnings could contribute to fewer accidents, impacting premiums positively.

- Climate Change and Extreme Weather Events: The increasing frequency of severe weather events like hailstorms can cause widespread damage to vehicles, leading to more claims and potentially impacting premiums.

- Regulation and Legal Reforms: Changes in Georgia’s legal system or insurance regulations could affect car insurance costs. For instance, reforms aimed at reducing frivolous lawsuits might lead to lower premiums.

Staying informed about car insurance trends and changes in auto insurance in Georgia can empower you to make informed decisions. By understanding the factors driving up costs and exploring ways to save, Georgia drivers can navigate the complexities of car insurance and find an affordable auto insurance plan that meets their needs.